This is a belated (and rough/short!) post for Effective Giving Spotlight week. The post isn’t meant to be a criticism of GWWC or of people who have taken the pledge[1] — just me sharing my thoughts in the hope that they’re useful to others or that I’ll get useful suggestions. Also, since I drafted this, there’s been a related discussion here.

I donate, and I’ve sometimes thought about taking a GWWC pledge, but haven’t taken one yet and don’t currently think I should. The TL;DR is that I’m worried about (1) runway and (2) my life changing in the future, such that donating more would be unsustainable or would trade off in bad-from-the-POV-of-my-EA-values with direct work.

Longer notes/thoughts

I’m currently prioritizing “direct work”. That doesn’t mean that I can’t donate (and in fact I do and enjoy doing it when I do), but I’m worried about committing to donating in a way that would lead me to make poor tradeoffs in the future. Signing the pledge seems like a serious commitment.

In particular, I’m thinking about:

1. Having enough runway[2]

- Runway seems important (and has been discussed a fair bit before, see e.g. here and more recently).

- … for potentially starting something on my own, or taking a poorly paid (or unpaid) opportunity to upskill

- E.g. going into a Master’s program, taking a sabbatical to see if I can build up a new idea, etc.

- … for epistemics & independence

- E.g. if I was worried about EV/CEA/the usefulness of my work, I can imagine leaving without another opportunity lined up, so I’m relatively free to consider what’s wrong at EV/CEA (otherwise this would be really stressful to think about). If I had no runway at all, I’d have a much harder time thinking about leaving. [Edit: see an elaboration on this point in this comment.]

- … for potentially starting something on my own, or taking a poorly paid (or unpaid) opportunity to upskill

- To the extent that donations trade off building runway, I should factor that in.

- I.e. if the alternative to donations right now is saving money, and I’m below where I should be for having enough runway, that means donations are in some sense more costly. It doesn’t mean I shouldn’t donate in any situation until I've hit my runway target, just that the bar is probably higher for me right now.

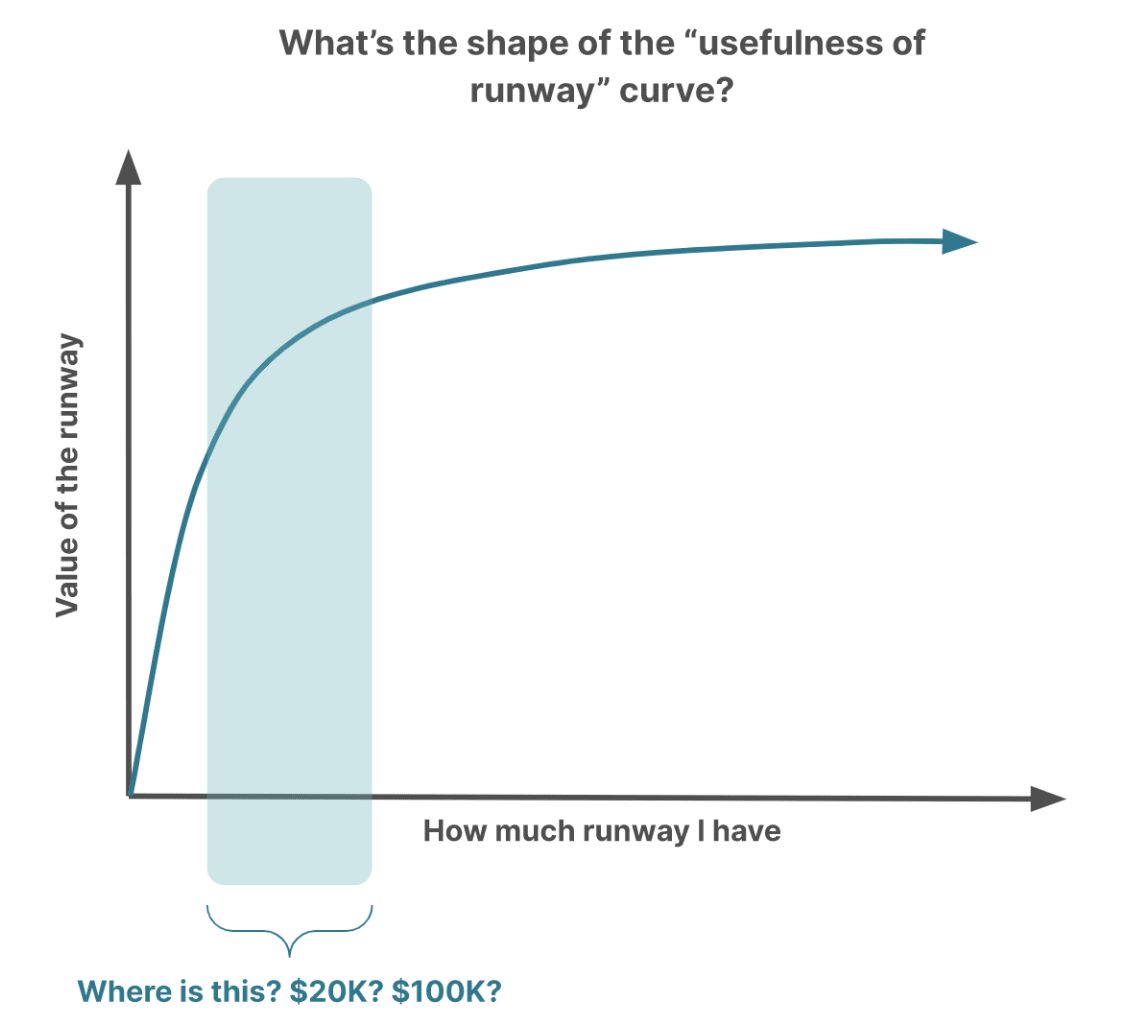

- How much runway someone should have (i.e. the shape of the “usefulness of runway” curve[3]) is confusing to me — I’d be interested in hearing what others think.

2. My life changing in the future, such that donating more would be unsustainable or would trade off in bad-from-the-POV-of-my-EA-values with direct work

- I have a family that I may need to support in some circumstances. I’ve thought about (not-too-unlikely) scenarios in the coming years where I might face a choice between having drastically less time for my work, spending significant amounts of money, or not fulfilling my family obligations in a way that I think is bad. (Being there for my family is one of my core values/goals.)

- And I probably want kids. If I have a child (or multiple children), I think there are many worlds where it would be better for me to be able to do something like hire a part-time nanny or pay for other services that would allow me to work more. (See this recent post!)

- Not committing to donating a certain amount every year might mean I can make better tradeoffs in situations like these.

3. Some worries about my thinking

- My reasoning might be motivated: I might be fooling myself into thinking that I shouldn’t take the pledge because that would be less stressful for me.

- Value drift: I’m worried that my future self might not donate for reasons that I don’t endorse. But I’m not too worried about that right now.

- ^

I'm really grateful to (and impressed by) the folks who've taken a donation pledge and who donate a lot.

- ^

Runway is less specifically related to the question of whether to take a pledge, vs. just the choice of whether I should donate at any given point, but it’s something I’m thinking about as I think about whether I should take a pledge.

- ^

Here's a sketch of what I mean:

I’m also not sure I’m even tracking the considerations that might be most important for determining this curve for myself or in general.

Thanks for sharing this! It's great to have some honest and open conversations about the GWWC pledge.

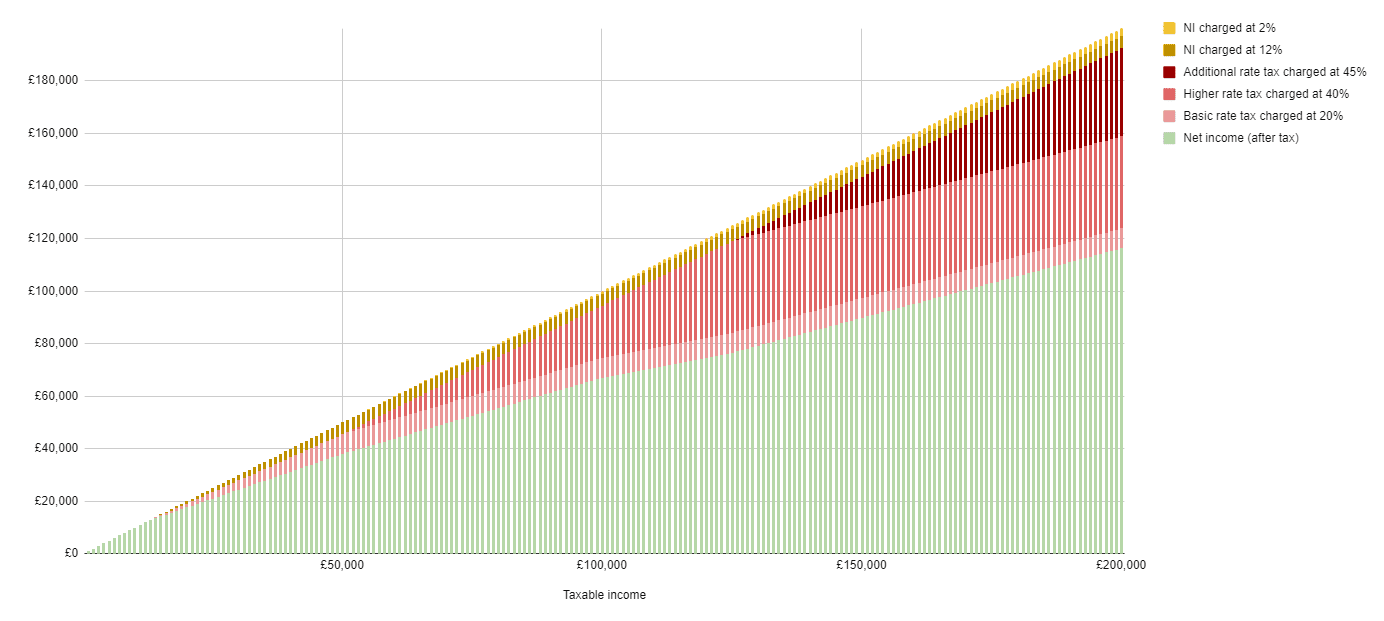

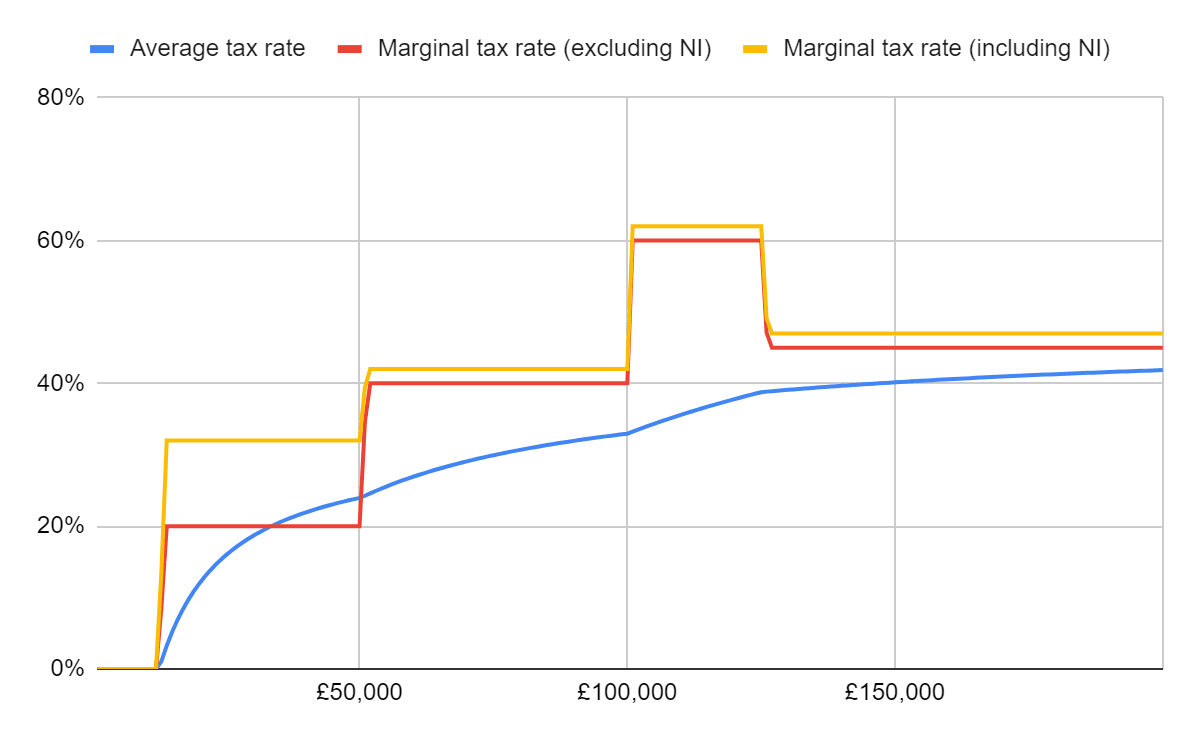

FWIW I think perceived wisdom is that around 6-12 months of living expenses is pretty good as an emergency fund, which might help in terms of your runway value curve. For example, that might look like £1.8k per month (which I think is roughly the UK average) x 6-12 = £10-20k. Ideally, this would be in instant access savings, rather than stocks (but this isn't true in my case).

Other thoughts: I think unless you expect your situation to change dramatically in the next year (e.g. you leave your job), it seems reasonable that you could both save for an emergency fund (at least partially) and donate 10%? For example, if you have a salary of £50k, that's a takehome salary of £37k, which might be broken down like:

Great comment - I'd add that usually GWWC pledges in the UK are based on pre tax so it wouldn't actually cost the full £5k. Donations reduce your income for income tax purposes (but not NI) - Payroll Giving (UK) or GAYE - EA Forum (effectivealtruism.org)

ie.

£50k salary

£3.75k donation which is grossed up by 25% from your taxes with gift aid to £5k

If you actually donated £5k then that would be a £7.5k total donation when grossed up with gift aid.

However, the higher rate tax (40%) band starts at ~£50k a year so every £1 donated above that costs 60p

(Working on a longer explainer on this which updates this piece UK Income Tax & Donations — EA Forum (effectivealtruism.org) but you can check out the underlying spreadsheet which create these graphs here: UK Income tax (including NI) - Google Sheets)

I love this breakdown, and it emphasises an important point (that was not mentioned in the post) that living expenses might actually be the highest variation, and often most critical factor in determining how much we might be capable of both giving and saving.

Oh yeah, a big one.

It was a combination of reading about Toby and the further pledge at the same time as reading some behavioural economics and learning about the hedonic treadmill that led me to switch our finances to "pay ourselves a living allowance" at a time when we were on a very low combined income and as our incomes grew so did both our savings and donations. It was because of the lower spend rate more than the savings that I felt able to take the risk of pursuing startups, big pay cuts to work in nonprofit sector, and we both took time off between jobs in 2019. It's certainly a privilege that not everyone has (e.g. things like living in a country with reasonable basic public healthcare certainly helps), but it's something that I've seen many peers not pursue (no matter how much they earn, just always spend what's in their account) and then look upon me enviably when I'm pursuing things that give me more meaning.

Thanks for sharing, Lizka! and thanks to everyone else for sharing their voices in the comments too!

I liked this post from Samie which talks about some factors for financial planning and security that are helping when thinking about donating - I liked the ideas about income protection insurance and thinking about financial goals.

I personally took a trial pledge for 3% of my income for a year before deciding I could really commit to the full GWWC Pledge. I've had ongoing health issues throughout my adulthood which at times meant I wasn't able to work full time and was concerned about my ability to potentially earn an income in the future - so it was a really big deal to me to sign a lifetime pledge.

There were a couple of things that pushed me over the edge to take the full pledge:

I think it's really up to each individual to figure out how much runway to save up, because our circumstances are all quite different (i.e. family, health, government policies, likelihood of changes to income level etc). I do think it was easier for me to sign a lifetime pledge because I have a family who are likely to be able to support me if things were really dire.

Taking the GWWC Pledge is a big commitment and I would recommend that people think carefully about it before doing so. I think a Trial Pledge is a great step and I'm really excited about the value of having people show that they're donating on a public register, even without the lifetime commitment, because this helps normalise effective giving and giving more broadly as a positive social norm!

(I work for GWWC but this was written in my personal capacity)

"Knowing that even on a modest income in Australia (or even on government benefits), I would still be really well off in comparison to the majority of people alive right now. My own health issues and suffering have been a big part of understanding how positively my donations could impact the lives of others, and I find that really personally motivating. "

This for me captures some of the important reasons for me why most people should take the pledge, nice one!

Thanks for sharing Grace. I think it's interesting you mention "that I could always resign if needed to". I'm also still on the fence of pledging, but I wonder if I should look at it similar as going vegan. Like, right now my goal is to be vegan for the rest of my life. So in a way I've pledged to that. But something could always happen later in life, perhaps health reasons, that would result in me 'resigning' from veganism.

I think of my veganism in the same way!

Thanks for writing this - it definitely makes sense to me and resonates with another discussion we had in the Berlin EA office recently on what counts as "disposable income".

I would just note three things:

And then relatedly:

And then finally, and a minor point:

In each scenario you mention, I think the correct trade off is "is the security for me not to suffer X more important than the benefit of donating this money?". So when it comes to caring for your family, I think it's fair enough to prioritise that pretty highly. But in this scenario, you could just carry on working at CEA while you do your job search, and I think it's pretty indulgent to say "the ability to resign immediately rather than do my job and look for other jobs on the side is worth more than the value of donating money to help people in extreme poverty". People become disillusioned in their jobs and start applying for other ones all the time, and I think you could do this as well, without undue hardship :-)

Thanks for engaging! Quick thoughts:

While we're talking about alternative pledges; I've considered taking a more general pledge to use some significant portion of the resources I have (and will have) for impartially altruistic purposes, with some carve-outs for other important values (like supporting family if something happens). I'd obviously need to operationalize it a lot better, and I haven't dedicated much time to thinking about it yet, but this seems more plausible to me right now.

I guess that if I were to prioritize thinking about this, I'd probably want to first think through the main goals of pledges and make sure a pledge like this is actually accomplishing something I think is important, instead of just allowing me to say something when pledges come up, etc. E.g. maybe the main benefit of a donation pledge is its public+memetic quality -- it encourages others to donate more. Or maybe it's about value drift, or something else, etc.

Thanks for clarifying, Lizka. Just for clarity on what follows - I absolutely don't think you're thinking this through in bad faith, so I don't want to come across as suggesting that. I do wonder if there might be some blind spots in your reasoning though, so I'm testing out the following to shine a light into those grey areas.

-

On your point 1 - what if was just "before my expected natural death/in my will"? I guess my point is: would you accept that it's reasonable to pledge to give away financial resources that you ultimately didn't need, after they had provided you with a safety net throughout your life?

More generally: I see your reasoning here but I think my reaction is still as follows. You want financial security to protect you in various scenarios, one of which is to protect against biases. There might be other ways to protect against these biases (your point 3.c is basically my point of view, for example - you definitely could blow the whistle on your employer anyway, even if you've donated some portion of your income over time, although I agree that this is harder on the margin if you're more financially dependent on your employer).

Ultimately, in each of the scenarios you outline, you're deciding whether to donate based on how you weigh one set of benefits (e.g. avoiding bias if your employer goes rogue) over another one (donating the money effectively).

Some of your scenarios seem completely reasonable to me (e.g. "I could donate but I want to make sure I can provide financial security to my family first."). Candidly, though, I think there is a strong whiff of motivated reasoning when the argument is something like "I could pledge to donate my money, but what if life expectancy has gone up to 150 in the future and I might need it?", or "I could pledge to donate my money, but what if my employer turns out to be net negative and I don't feel able to do anything about it because I didn't keep my resources to get financial security?".

It seems to me that if we allow this level of speculation in the justifications for not donating, we have to conclude that no one should ever be expected to donate anything, because clearly we could always construct some plausible scenario where they later regret doing that. (To put it a different way, this line of reasoning seems very vulnerable to reductio ad absurdum.)

In reality, lots of people donate 1-10% of their income, and I have never actually heard of someone who suffered significant hardship and said "if only I had not donated that money, I'd have been fine" (although NB: these people clearly could exist - I'm just sceptical that it's true in the vast majority of cases).

For one thing, most affluent people in high-income countries spend at least 1-10% of their income on stuff they clearly don't need. So for these arguments to be convincing, I'd also need to be convinced that you are spending 100% of your income either on essentials or on savings or investments. I have no idea about your financial circumstances, so that could be true. In my own life, it definitely isn't true. So if I said "well, I could donate 10% of my income, but that would undermine my financial security", this would be a false choice. I'd be better off not getting Ubers or takeaway food so often, joining a cheaper gym, drinking less wine and putting that money into savings; and donating the final 10% anyway. (Another way of putting this - people tend to theorise about this as if they are making decisions on the margin, but we are almost never, ever, ever actually acting on the margin.)

In summary, I guess every time we decide to keep a unit of resources to ourselves rather than donate it, we tell ourselves some form of justification for that. It's just that I tend to view justifications that are second- or third-order insurances with suspicion, because they look and sound a lot like "I'm going to keep even the final 1% of my income to myself but it's not for my own benefit, it's for impact".

One potential crux here is: in what percentage of potential universes should my runway be long enough? 100 percent is impossible, and 99.999999 percent is impossible too, with a possible exception for HNW individuals.

One potential diagnostic here (in general, not commenting on anyone's particular situation): if someone concludes that they need a very high coverage runway, how much of their current income are they devoting to getting there?

If I conclude that I needed 99 percent coverage, the risk of the runway not being complete when I needed it would be significantly higher than the risk of the completed runway proving insufficient. Is the amount I'm contributing to my runway fund consistent with that risk assessment, or am I spending a lot on Ubers and takeout, nice gyms and wines, etc.? If someone who is currently earning is stowing away a large fraction of their current income into runway, that is a costly signal that they really do prioritize the risk of insufficient runway, and are less likely to be engaged in motivated reasoning when they decide not to donate much now due to runway concerns.

I might be underthinking this but to me the 10% pledge is only about acknowledging that I earn significantly above the minimum wage in the region and hence giving up on 10% will likely not have a significant effect on my wellbeing.

Then for factoring in the tradeoffs related to direct work, a starting point I could think of so far is if funding would be available to cover them. If you think about it, you decided to take a tradeoff to pursue a direct work opportunity. You could have also just kept earning and started donating the difference to a fund. Now imagine someone else comes with a funding application to the same fund. This other project has the exact same expected returns as your direct work project. The only difference is that this other project requires funding. Assume that the amount required is the same as the difference you'd donate. You might see where this goes. The two projects are equivalent from the fund's perspective (for each project to get done the fund is worse off by X money). This means - if I did not mess it up - you taking the tradeoff for the project is at least as good as donating the difference to the fund (assuming the fund would be happy to trade off this amount of money for the project you are doing).

So I'm not sure if taking a tradeoff like this would technically count for the pledge, but I think the result would be at least as good as donating the difference to a given fund. And so far I assumed that this is what matters.

(Note that I also had a likely not too successful attempt of writing up this idea from a different perspective)

I believe GWWC do include 'income you have sacrificed to do direct work' in their pledge. (Correct me if I'm wrong, GWWC folks.)

Although, of course, your main argument (which I endorse) would still be true - you'd almost certainly still be earning substantially above the minimum wage in your region, and could most probably still give up 10% of your income, without materially affecting your wellbeing. So it's a bit debatable if you should then feel like you've "fulfilled a pledge" by doing direct work at a lower salary.

(Excuse the brevity, typing on my phone). The spirit/norm is:

TL;DR Spirit of the pledge: If a voluntary pre-tax donation/salary sacrifice can be the means for which someone fulfils their pledge if it’s basically a different way of transacting a voluntary donation.

Like if you owe a friend $20 and then you use your card to pay for $100 for a dinner for the both of you it might be easier for him to just pay you $30 (instead of him paying you $50 and you then giving him $20).

The distinction is important because (a) it’s good to encourage people to make high-impact career trade offs, but (a) GWWC isn’t/shouldn’t be about starting to track all of people’s impact decisions in one place and converting all volunteering and lower (or hypothetically lower based on glancing at Glassdor) paying jobs into $ so you can then donate less actual dollars. It’s about recognising if you’re in a relatively well off financial position and voluntarily using your available financial resources to help others as effectively as you can.

Allowing some flexibility for means of donation (eg stock transfer, salary sacrifice, payroll giving) where it’s simpler or more tax efficient is better than saying it always has to be cash, but getting into the game of hard to measure non currency counterfactuals is a slippery slope that would undermine the advantages of a simple common norm.

Similarly if someone were to donate $10k of stock that they had good reasons to believe was about to lose half its value (i.e. knowing it’d only be worth half as much to themselves or the charity) and then it subsequently did lose half its value before the charity could liquidate it, then it would be in the spirit of the pledge to think about that as a $5k donation (regardless of what the taxman thinks). (Although the kind of donor that’s donating large amounts of stock and is very bought into the spirit of the pledge is likely well above the 10% anyway and wouldn’t be faulted for not finessing their pledge calculation to account for this if they’re so far above their 10% that it’s immaterial to whether they’re on track to meet their pledge or not).

Thanks for clarifying, I think the arguments makes sense! The FAQ is clear on this and it’s good to see some of it’s background.

I can accept that it’s a tricky situation and the overall best way to handle it is to consider a resign.

Further to my lunch example. If you said “I’m buying lunch!” or “Lunch is on me!” then you still owe then $20.

This does not seem like a very plausible interpretation of the actual words in the pledge, and the GWWC FAQ is quite clear on this matter:

Is this true GWWC? I didn't realise that sacrificed income counted.

Not exactly, depending on what someone means by "sacrificed income". See my comment clarifying this. Essentially "salary sacrifice" (a form of payroll giving where you take home less pay for some kind of benefit including a donation to a charity; or equivalent arrangements) is different to "choosing a lower paying job for impact reasons". The key here is it's voluntary, revocable, has a specific monetary value, and the donation is very specifically one that would count towards a pledge.

Yes, the wellbeing argument still applies even after the paycut if you’re still substantially above the regional minimum. But if you compare it to your original wage, given that you only committed to a barely noticable sacrifice, which the paycut itself likely even surpasses signifficantly, that additional 10% might just be too big of an ask.

However if one is also just fine with earning around the lower wage and even donating from that, then I think considering something like taking the further pledge may also be an interesting idea.

Thanks for sharing Lizka! I appreciate you sharing these considerations :)

Personally, I donated at roughly the 10% amount for several years before taking the pledge (and at some point in the process I actually thought I had but when I realised I in fact hadn't in 2016 I then did it on the spot lest I forget again). I've definitely leaned into the "lifetime" part of the wording at points and after taking the pledge I had years where I gave below 10% (e.g. when working on my startup and taking home below minimum wage) and others where I have far exceeded that amount. While I've not taken the Further Pledge it is more similar to the way I think about my giving/living expenses.

I'm interested in hearing from people who might feel similarly about the full lifetime 10% pledge as to whether they have considered using the Trial Pledge for shorter periods or smaller amounts. And for those who have, how'd they find the experience? And those who haven't, why not? (Personally, I hadn't heard of it before I took the full pledge, so it might simply be awareness.)

FWIW almost half the new pledges each year are Trial Pledges.

You can think of the GWWC pledge as analogous to marriage, and that would make the trial pledge something like moving in together. In the romance analogy, some friends of mine who are reasonably averse to lifelong commitments do "handfasting", or intentionally not lifelong partnerships. A thought I've had for a while is that the Trial Pledge, by virtue of its name if nothing else, does poorly in the position of handfasting, where often the intention is never to get married (/ take the pledge).

(Anyway, all academic for me as I'm crazy enough to have done the lifelong pledge.)

I also like these analogies!

Does the marriage analogy as you perceive it include that breaking the pledge further down the line is pretty common and socially okay, but also that it's a serious thing and breaking it is not to be taken lightly?

This is roughly how I view it, except I want to view the level of commitment for the GWWC pledge roughly the way the median of Western society views marriage, as opposed to (e.g.) how EAs view marriage.

I think that captures it about as well as I could. One thing I'd add is that similar to marriage my preferred norm is to formally resign if you no longer intend to stick with it (and not just start ghosting if you're no longer vibing).

Less this:

More this:

...but then, I'd also like more marriages to end in a way that more peaceful and respectful than is common.

100% agree that the "Trial Pledge" branding doesn't mesh well with those who are more serious than trialing but do not feel called to the 10%/life pledge. If the GWWC pledge is analogized to marriage, the Trial Pledge covers everything from the analogy to entering into a committed relationship (pledging 1% for a year) to the analogy to temporary marriages (pledging 10% for a time period) and the analogy to a registered domestic partnership (pledging, say, 5% for life).[1]

By "domestic partnerships," I mean a legally recognized relationship status that can be seen as less than marriage. In the US, these statuses were often initially created to give some recognition to same-sex relationships, but even after marriage became available to all, these statuses remain on the books as an option for all relationships in some jurisdictions.

I like the analogies! I've used the former one before but I like the addition of "moving in together" analogy for the trial pledge.

Also regarding the name, it was "Try Giving Pledge" before and I think the "Trial Pledge" adjustment is a slight improvement, but really don't think it's been nailed. Would be super interested in alternative ideas and possible consequences of those names.

Babble:

Regarding "How much runway someone should have".

I'd very much plug spending time actually crunching the numbers and using some financial planning resources (e.g. Yield & Spread). Huge amount of peace of mind when you actually calculate different scenarios.

Literally building a spreadsheet and writing out assumptions helps a lot. I remember going through this with my partner in our early 20s it involved hard calls but once you actually see the numbers it helps. It's going to be so personal though like how happy you are with rice and beans, if you have a family/friend you could crash with for 3 months if necessary etc.

I am still on the trial pledge and have been for a while now. I think promises really matter and so one shouldn't make one that one can't keep. I am sad that my pledge number is rising and that I don't get a bad, but I think this is better for me overall.

Thanks for writing this.

TLDR: I am glad that I am not the only one who thinks "I'd like to help, but I want to make sure I have enough financial runway first."

(The rest of this comment is just my musings and explorations.)

I'm glad you wrote this. I've had vaguely similar thoughts bouncing around in my head during the past few days of seeing so much talk about giving.

I've donated a small amount of money over the years (≈8% of my income one year, and ≈1% another year), but I've never taken a pledge, and for most of my adult life I've not felt as financially secure as I would like. I feel a vague sense of pressure that effective giving is something I should do, and that it is something other people will think more highly of me for. But I've crunched numbers, and I have a spreadsheet, and I know a decent amount about personal finance. My rough narrative is something like this: there are bad things that have a reasonable chance of occurring in my life. If I have enough money available, then most of these things will be an annoyance, or a minor setback, or a negligible cost to me. If I do not have enough money available, these most of things will be a major setback, or will irrevocably alter my life path for the worse, or make other things much harder for me.

I would also like to retire someday. I assume that I will eventually reach an age where I lack the energy or motivation to do stuff, and I don't want to be in a situation in which I am forced to choose between doing a miserable job and not being able to afford decent food, clothing, and shelter.

If I had an in demand skill that could easily get me a well-paying job, or if I had family wealth to rely on, or if I had an excellent professional network from a well-reputed university... well, the more of these things one has, the less risk-averse one has to be.[1] But in general I feel a great sense of financial precarity, and currently I am not confident that I will have enough money in the future to provide a modestly comfortable life for myself.

In brief, I want to make sure that I am taken care of. Any money above and beyond that I am happy to get rid off (such as donating it at the end of my life, or doing donations after a few years of earning good money).

For legal citizens, it’s less risky to drive above the speed limit. For married people with two incomes that share expenses, it's less risky to quit one job to start another. For people with a highly in-demand skillset, it is less risky to take time off work to travel. For students not relying on scholarships, it’s less risky to skip class. For people with non-abusive parents, it's less risky to live with family. And so on.

Thanks for writing this, I found many of these points relatable. As I read the post I found it a little surprising that I haven’t seen more of this kind of discussion.

The epistemics and independence point feels particularly important - I think this is one of the main factors that makes me want to build more runway. I don’t have a very principled view of how much runway is “reasonable”, if people have numbers in mind I’d love to see them.

My best guess is that you want to have enough money that you can see yourself transitioning to a reasonable job outside of EA, in a way that's not financially scary, plus some buffer.

For people roughly in my shoes (childless, basically healthy, no significant dependents, but also definitely can't rely on family or other people outside of the EA community for financial stability), I'd guess that this looks like ~6-24 months of consumption in your early-mid twenties, and ~18-36 months in your late twenties or early thirties. [1]

Naive extrapolation suggests higher numbers for older people, but I've never been older, and I'm not sure how useful speculation is here.

My guess is that people with more reliable sources of financial support (most obviously family, but also religious communities, or living in countries with more reliable social safety nets than the US) can get away with lower savings, and people with a higher probability of large variable expenses (eg older, chronic illnesses that sometimes flare up in expensive ways) should have more savings.

I'm not sure which direction dependents should change the numbers. On the one hand there's a clear case for wanting a higher buffer (generally, people with kids want more safety), but on the other, often people with dependents effectively have other forms of insurance (eg a wage-earning partner, or one who can go back to the workforce, and/or governmental subsidies for unemployment).

I would also guess that considerations change quite a bit when someone is close to retirement.

I suspect my numbers are higher/more conservative than other EAs, particularly public commentators. I think this is partially due to me thinking the costs of high runway isn't as high as them (I mostly model it as costing time value of holding the money rather than donating, instead of the whole lump sum), partially because it's easier for me to see realistic worlds where I'll just be screwed if I'm both unemployed and don't have remaining savings, and partially because I'm cowardly.

The reasoning for variable and increasing numbers with age is that younger people usually have more flexibility to change jobs (getting an EA job right out of college and quitting after a year is almost strictly better for career capital than taking a gap year, say), as well as greater emotional and practical ability to change lifestyles without it being as scary. More experienced people also take longer to retrain and may have a lower number of jobs that they're excited about.

"but I've never been older" - best quote of the day ;)

Thanks for posting this, Lizka!

I think your reflection points to some tradeoffs about the way the GWWC pledge is currently structured. Before I mention them, I should emphasize that they are tradeoffs, and addressing them would mean compromising on other endpoints (most notably the value of simplicity).

Thank you for sharing. This felt very personally relevant. I also haven't taken the pledge. I very nearly did in 2016. I go back on forth on whether and when I should take it. There are so many considerations at play.

How much am I willing/able to sacrifice my wealth and financial security alongside sacrifices made for my direct work? Would/will I have as much direct impact without my savings/passive income potential? I'd be more risk-averse and less likely to address 'funding market failures'. Could I give more and give better later on that now? How much is motivated reasoning because I am very averse to spending on most things... etc

I also find it a little hard to talk about with people who have taken the pledge without feeling worried that I will be judged for being selfish or just feeling selfish and bad etc.

Related to that, I would really like someone to make a decision tree, guesstimate model, or similar for people to determine when and whether someone should take the pledge or donate money.

Related to this desire for when to give analysis, I would also like some way of upvoting potential posts or project (and even funding them), perhaps hosted on or linked to the EA forum. The situation feels like a potential coincidence of wants problem. I think I would pay maybe 100usd for a good post on this topic, if easy. I suspect that a lot of people would also be willing to do this (but not sure). I think someone else would take the opportunity to write the post/make the model if they knew there was demand, but the opportunity/demand is not easily advertised/aggregated etc.

Thanks for the post, Lizka!

To account for kids, the concept of equivalised income can be useful:

For a household with 2 adults and 2 kids under 14, the effective size of the household would be 2.1 (= 1 + 0.5 + 2*0.3), which, for 2 adults earning money, suggests one would only have to multiply the runway respecting living solo by 1.05 (= 2.1/2).

I prefer to have more than the above suggests for caution, always considering a weight of 1 per person. My target runway is 6 times (= 2*(1 + 0.5)*2) the global real GDP per capita (in Portugal, 69.4 k€), which would allow me to live without any earnings for 2 years with 0.5 dependents with 2 times the global real GDP per capita per person per year. I have been donating (so far, about 20 % of my all-time income) as I build my runway up to that level, and plan to donate everything above that once I reach it.

I'm curious as to why you used the global real GDP per capita in your calculations. Given that the purpose of runway is to serve as a medium-term buffer, it seems like the level of expenses one would expect while using runway, or the median salary where one lives, might be used to calculate how much runway one had.

(Your donation level and plans are awesome, by the way -- this is written as background to the broader readership, not a suggestion that you change your approach!)

Thanks for asking, Jason!

2 times the global real GDP per capita is 35 k 2017-$ (= 2*17.5*10^3), which is quite similar to the 36 k 2017-$ respecting the real GDP per capita of Portugal (23.1 k€ at current prices in Portugal), where I live. I also think it makes sense to connect the runway to a global quantity, such that my position in the global income distribution is roughly fixed. 23.1 k€/year in Portugal means I am richer than 97.5 % of people. I find it hard to make a case that I need more, given my annual expenses so far have been much lower (like 1/3 of global real GDP per capita). The expenses would significantly increase if I did not live with family (working remotely), but I have also lived alone for 1 year in Stockholm spending around the global real GDP per capita (accounting for both my spending, and family support). On the other hand, maybe spending more will be helpful at some point, namely if I start a family, so 2 times the global real GDP per capita seems better.

Thanks for the kind words!

I think I misread "6 times (= 2*(1 + 0.5)*2) the global real GDP per capita (in Portugal, 69.4 k€)." You meant that the runway was 69.4k€; I applied the parenthetical to "the global real GDP per capita" and assumed a significantly higher runaway! These are the downsides of commenting on the Forum via phone while taking care of a toddler....