UPDATE 2 FEBRUARY 2023: I've updated a new and streamlined version of the “FI-lanthropy Calculator” based on the comments of many.

REQUEST

I am soliciting feedback on a tool I have made entitled the "FI-lanthropy Calculator". The target audience includes existing or aspiring members of the FIRE movement (Financial Independence Retire Early). They may use this calculator to explore the impact of taking a giving pledge both to their FI timeline and their retirement portfolio.

This tool is meant to be simple to use and easy to digest. It is not a comprehensive financial plan, but more so a way to ‘whet the appetite’ for giving in general. I view this tool as a companion to, say, The Life You Can Save’s Impact Calculator. We know this is not exact, but it’s a good place to see tangible examples of how much good you can do.

I’d like to know:

- If you find this tool helpful and/or informative

- If you think it is missing anything crucial (keeping in mind I want to keep it relatively simple)

- If there are any major errors I’ve missed

RATIONALE

There is a growing movement within the FIRE community of people who are focused on giving back and looking for ways in which they can successfully find financial independence but also create space to help others. This can be seen through the growing number of members in the Socially Conscious FIRE facebook group (now at ~9,000 members, up from <1,000 when I joined in May 2020). We also see true leaders within the Financial Independence community continuing to lean into this space include: Pete Adeney of Mr. Money Mustache advocates for Effective Altruism directly on his blog, Tanja Hester of Our Next Life has written Wallet Activism, and Vicki Robin has her podcast What Could Possibly Go Right. (The last two are not EA focused, but have had a very large influence on getting people to think more about charitable giving in general.)

I believe there is a large audience here for the EA community to reach (Mr. Money Mustache’s blog has had tens of millions of visitors), with advocates already in place. My hope is to provide more tools and resources for the FI community to consider some of the EA practices, largely Earn to Give and Invest to Give.

While some may feel that the communities clash (FIRE focuses on bettering oneself while EA focuses on bettering others), I believe that there are more synergies than we might think:

- FIRE folks are optimizers: They ensure that each dollar is working for them, and that little money is wasted. They believe that each dollar they spend or save goes to a useful cause. It is likely FIRE followers will more readily understand the importance of effective charitable donations, knowing their dollar does the most good possible.

- FIRE folks spend time to understand what makes them happy: FIRE followers, if diligent, have spent a significant amount of time evaluating the marginal benefit of spending more money on themselves once their basic needs are met. And thus, if they have money to satisfy their basic needs and more, there is an opportunity to share this money with others.

- FIRE folks who are close to retiring early or have already retired are looking for meaning: While it’s true that many people are focused on the journey to getting to early retirement, at some point the question will come up “What is the point of all this?”. And many find that it’s less about quitting their full time work and more about finding meaning in life. And quitting your job gives you a lot more space to think through that. Vicki Robin uses the Hero’s Journey to explain this concept exceptionally well in this video.

- Many seek FI without the need to RE: Many folks don’t necessarily want to retire early, they just want the ability to become Financially Independent. Being FI allows you to make life changes more easily as you are not obliged to stick with a certain job that provides a specific income level. Many who reach partial FI, or Coast FI, start to make big life changes, having achieved a baseline of financial security. And often that means leaning into more purposeful work that perhaps pays less. For example, someone who leaves a high paying job in tech to start an effective charity.

QUICK SUMMARY OF INSIGHTS

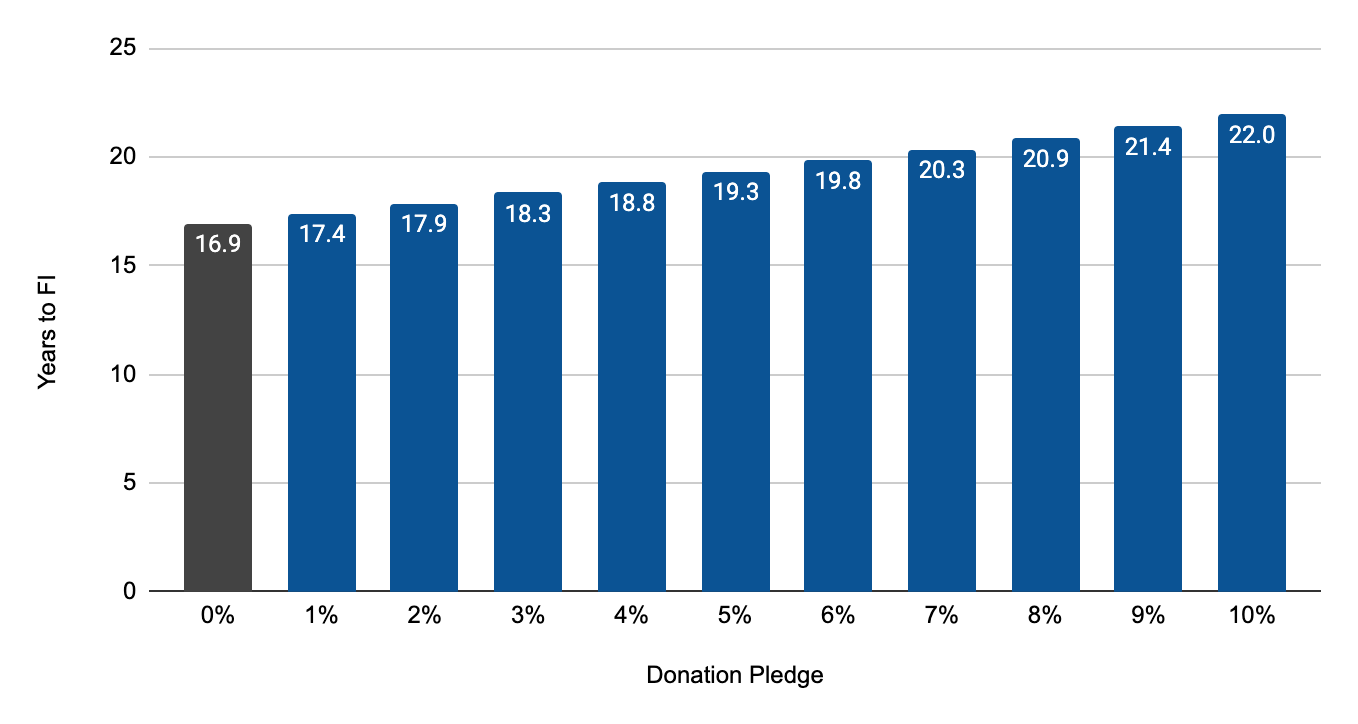

Let's walk through an example: Let's say you make $70,000 a year after taxes, and spend $40,000 a year, meaning you have a personal savings rate of 43%. You already have $100,000 in your investment portfolio. You have not yet taken a Giving Pledge but are considering donating 1% on a go-forward basis.

Using the Fi-lanthropy Calculator, you would find that pledging 1% would increase your FI timeline by 0.5 years, or 6 months of working. In the scheme of 17+ years of working, this may be noticeable but not substantial.

Assuming your income and expenses remained the same, it means you would donate $700 a year, or $21,000 over the course of 30 years. According to The Life You Can Save's Impact calculator, this means you could help to purchase 10,500 bednets to protect those living in malaria-stricken areas from infected mosquitos, and help save 5 lives.

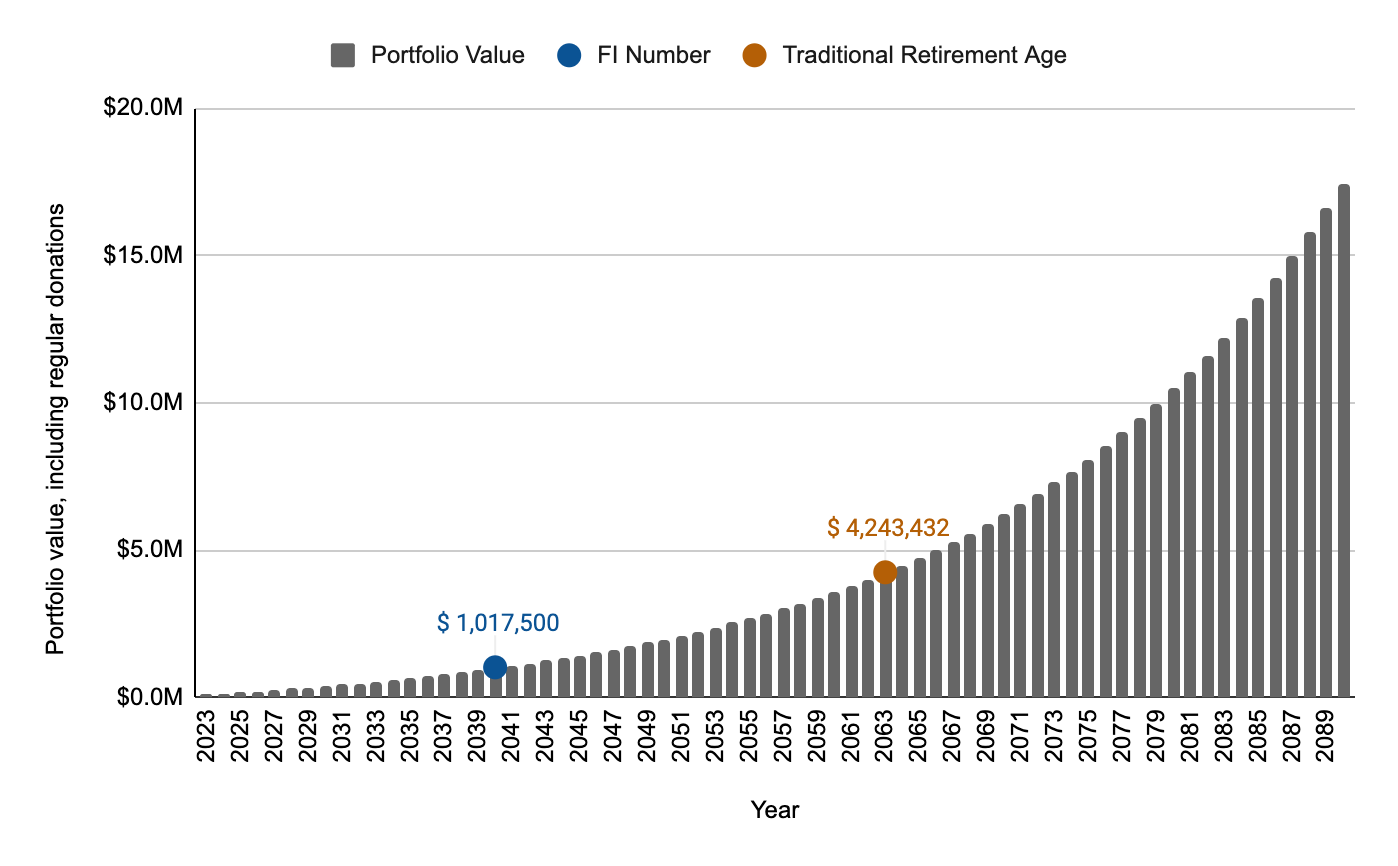

You would still be reach early retirement in 17+ years, with an estimated portfolio value of $1,017,500, or you may choose to keep working to earn active income. Either way, you have a nest egg to donate upon your death in addition to regular donations.

Donating even just the baseline target FI number, again $1,017,500, would help purchase 508,750 bednets, or 254 lives saved based on today's estimates.

There are of course a number of assumptions here, and you may read more about those directly in the calculator.

TECHNICAL COMMENTARY

I made this in Google Sheets because my technical capabilities only extend this far. I am aware that making this an online tool with a slightly sexier design would improve the user experience.

With that said, if there are any data scientists, engineers, or developers who are reading this who would be looking to partner on this, please reach out.

For those of you familiar with Networthify’s Early Retirement Calculator (an extremely popular FIRE calculator featured in the community often), the Fi-lanthropy Calculator uses similar assumptions.

PERSONAL BACKGROUND

I am a member of both the FIRE and EA communities. I retired from my corporate real estate job 3 years ago at the age of 32. Now I live an early retiree lifestyle and also run my nonprofit Yield & Spread. We teach working adults how to learn and invest to build wealth, and we distribute all our profits after operating costs to effective charities. We are working towards creating more content around financial independence and giving, starting with this Fi-lanthropy calculator.

I am a personal believer that financial literacy is another superpower we can unlock to do more good in this world. The better we can take care of ourselves, the more we can create space for others. I continue to see requests for Personal Finance support (as you can see from this EA Forum post), and I hope to help in this space as much as I can.

This is my first time writing an EA forum post.

SUMMARY

I believe having more tangible tools that people can use to calculate their donation impact is helpful, especially in the context of personal finance. I welcome your feedback on this Fi-lanthropy calculator, and any other thoughts on desired content.

This is really cool! As someone who's been doing these calculations in a somewhat haphazard way using a mix of pen and paper, spreadsheets, and Python scripts for years, it's nice to see someone put in the work to create a polished product that others can use.

Something that I've been meaning to incorporate to my estimates and that would be a killer feature for an app like this is a reasonable projection of future earnings, under the assumption that you'll get promoted / switch career paths at the average rate for someone in your current position. Sprinkle a bit of uncertainty on top, and you can get out a nice probability distribution over "time at FI" and "total money donated".

This is a thoughtful comment. And what you are requesting is also often missing from many FIRE calculators. Perhaps there is a simple work around to this...like including a formula that says "My salary will increase by X every Y years". Obviously this is hard to predict, but does offer the user a little more flexibility if they assume their income will go up and want to play around with the numbers. At the same time, we are also assuming the user's expenses remain the same, which we know is not necessarily true as well. So trying to find that balance between simple and flexible. I will think on this more. Thank you.

Javier, I think it would be extremely cool if someone made this projections tool based on salary data aggregated from levels.fyi

As for the direct, object-level questions you make: Yes, it's very helpful and informative, and I don't see any major errors. In fact, the "additional funds required" and "extra time to FIRE" charts are very useful, and to my knowledge, haven't been done before. Congrats!

As for something missing, something I sometimes get requested to calculate is how great is the impact of donating now vs. donating later. Like, what if I want to extra-quickly grow my nest egg for 6-10 years or until 60-80% of the way into FI (amounts to be written-in, of course), before donating? Would that lower my donations much? That is, the reverse of "how much delay for this amount of donations?".

As general commentary / small things / nitpicks:

Extremely helpful commentary. I've updated the charts with your recommended formula per comment No. 4, and given some extra commentary around No. 2 and 3. I'll have to give some more thought to your comments about "donating now vs. donating later" and incorporating this level of flexibility. There's probably a few ways of doing this -- and perhaps this is best done in a separate section or separate calculator even. It also encourages me think a bit more about audience for this tool -- if you are new to giving then my gut tells me something more simple will help someone get onto this path more easily...whereas a tool that is more flexible with more options for donation strategy may be better for someone well versed in this space. I think there is space for both. So again, will think on this one more. Would be very happy to chat with another early retiree directly if you are interested, @Alejandro Ruiz

Thanks for sharing! I've had many conversations about this and will definitely be sharing this with people in the future 😀

I'm a big fan of both EA and FIRE, so this is awesome!

One way the tool could be improved is by allowing to adjust for-tax deductibility of donations.

I'm not quite sure how the calculator would be adjusted, but the relevant metrics seem to be.

The distinction between if it applies to net or gross income might be necessary, because countries differ to the specification of tax-deductibility of donations.

Thanks for this. I agree that a tool like this would be extremely helpful, but frankly, extremely challenging to build. There are so many scenarios that would influence deductibility in any given year, let alone over time. And the calculator begins with entering an assumed income after taxes. Even if I were to include a line item that says % of donations that are tax-deductible, having the user accurately calculate or predict that on their own would be extremely challenging. It would also impact their income and expenses. With that said, I am also interested in these types of insights as I think they would be incredibly powerful -- but just much harder to "productize" into one tool.

Thanks for this! One thing I noticed is there is an assumption you'll continue to donate 10% of your current salary even after retirement - it would be worth having that as a toggle to turn that off, since the GWWC pledge does say "until I retire". That may make giving more appealing as well, because giving 10% forever requires longer timelines than giving 10% until retirement - when I did the calcs in my own spreadsheet I only increased my working timeline by about 10% by committing to give 10% until retiring.

Admittedly, now I'm rethinking the whole "retire early" thing entirely given the impact of direct work, but this outside the scope of one spreadsheet :P

As another early retiree - at least, I was, for some time, before I un-retired (hopefully temporarily) to pursue an expensive startup project, as a funder - I think you underestimate the power of the FIRE's income. By the time most of us are ready to "pull the plug", the usual question is not, "How probable is that I never run out of money?", but "How much time did I overspent working, since this safety margin is, with benefit of hindsight, obviously excessive?". Thus, most FIRE types should have more than enough to maintain donation rate, and probably increase it.

See for example, https://www.mrmoneymustache.com/2022/07/18/never-run-out-of-money/

Thank you! I question if the words "until I retire" is a steadfast rule or more of a guideline from the GWWC community simply because it's easier for people to digest. I imagine it is easier to come up with a donation amount based off of your current and predicted active income, whereas it can be harder to predict that donation rate once you are an "early retiree"...which I know from personal experience as I don't really have a true income to base my 10% on. So to me this seems more of a messaging point of friction. I guess the question then is, should early retirees continue to donate at the same rate once they retire? Or rather, should any retiree at any age continue to donate at the same rate once they retire? My perspective is this can be harder with unpredictable income, but if you can build it into your financial plan early on, then you are in a much better place to continue donating on a regular basis, even once you lose the active income. So, I'm tempted to not have the option to toggle it off, but there may be value in showing the difference in portfolio value and FI timeline. I welcome more feedback!

This is a great idea! I was, indeed, surprised by how few extra years were added by even a 10% pledge.

Minor comment: I didn't notice at first that typing in more than 10% breaks some of the calculations; it would be nice if this were more obvious (e.g. by clearing the fields that can't be calculated).

Thanks. I've gotten this feedback more than once so will address it!

I love this Rebecca!

The only thing I'd want to see changed is to add a pledge % cell into the FI table at the top, so you can play around with the percentage right from the start.

I'm assuming people visiting the calculator will have at least some idea of what they're about to look at.

Awesome! I'm glad to see these two communities connecting, I think there's a lot of potential for cross-pollination. You might be interested in this thread, and this post. I'd love to see these ideas popularized in EA, as I think people who have flexibility and agency can achieve great things.

The tool looks great, one little suggestion is to merge the cells with the link and the ones to the right of it:

so that the link is clickable :)

Updated! And yes, I left a comment on the Personal Finance for EA thread. Thank you for highlighting that other one too.

I think it looks really nice and it easy to use. I like this a lot, especially the emphasis on how investing early can enable to you give increasingly large amounts in the future.

Off the top of my head the only changes I would make would be to either

There's been some updated studies completed since the Trinity Study proving that you may actually be able to withdraw even more than 4% safely. And that it really depends mostly on when you retire, what your portfolio valuation is upon retirement, and what happens to that valuation in those first few years not earning active income. Michael Kitces talks about it here and here. So i still feel confident to leave the base number at 4% and if people want to change it they can.

I further clarified DONATION RATE IMPACT TO TOTAL FI NUMBER

Thanks for the links. I'll explore those, and maybe even end up updating an overly conservative perspective on safe withdrawal rates and long retirements. :)

Wanted to share with readers of this post that Yield & Spread has added a free 1:1 coaching program for do-gooders who want to explore and improve their personal finances. We are calling for applicants in this post. If you found the FI-lanthropy calculator helpful, please consider applying.

Thanks for sharing this. It's such an interesting idea! I think the bit about donating your estate could be especially significant for FIRE & EA folks, although the impact of course materializes in the future. Perhaps those close to retirement could be persuaded to move their assets into a charitable remainder trust or charitable annuity?